Original post here was June 2013. Or, jump to the Nov 2015 update below.

Latest in my series Let patients help, cost-cutting edition

I’ve blogged several times about the greatest truth I’ve learned about the business of medicine. It’s the title of a 2006 Health Affairs article by Princeton economist Uwe Reinhardt: The Pricing of US Hospital Services: Chaos, Behind a Veil of Secrecy.

The cost chart at right shows what’s happened since Reinhardt’s paper appeared, in the middle of the chart. It’s what you’d expect if slush is flowing around with nobody watching.

Today I was reminded that it ain’t just hospitals. :-)

______

Last week I got my annual checkup. There were two separate problems in my hospital’s appointment system, so I ended up leaving too late to get the simple lab work my doctor had ordered; I said I’d get it done at a local lab.

Today I visited AnyLabTestNow, a chain with a local office. I called ahead, and for walk-in self-pay, it’s $49 for the chemistry panel I needed (Calcium, CO2, etc) and $49 for the cholesterol, total $98. And a $10 off coupon, on the site! Just $88.

Or not.

I checked with my insurance company, and the blood work is covered 100% as part of a normal checkup, because “The doctor diagnosed the test right” (her words – i.e., he ordered the test using the right ICD-9 code).

BUT, the lady was careful to point out “This is not a determination of benefits, just a description of services.” How’s that for malarkey? “We’re not saying you WILL be reimbursed when you submit the claim – I’m just telling you what the policy says.” But she’s required to say it, because the company that denies claims is not accessible through customer service and might possibly deny the claim, even though she said it should be covered.

And I am not allowed to talk to someone who does know, right now when I need the service, to actually find out. The only way to be sure is to file a “predetermination” and wait a week. If I don’t and the determiner says no later, I’m stuck with it.

And I can’t send it to the “determiner” (to invent a George W word); I have to send it to the service company, who in turn forwards it to the determiners. Then the uncontrollable delay starts – she said “We try our best to get it back in 5 days, we really do, but sometimes we can’t.”

Guess who’s holding all the cards and all the power behind that veil of secrecy?

It ain’t me the watchful consumer, and it ain’t even the nice customer service lady. She, meanwhile, explained that “It’s not a person who makes the decision – it’s the computer.” I explained that if she’s been fed that line of malarkey, there’s more funny business going on, because somebody puts the rules in the computer and I want to talk to someone who knows what the rules are. So I can be responsible about medical costs. Which nobody else seems to want to do, in this picture. :-)

Anyway, I got the blood taken, and in a couple of days the results will be sent to him and visible to me online.

But really – no, really – what did this cost?

Even though insurance paid, I care about costs, especially since my premium went up 20% last year, even though I didn’t file a penny of claims; I still want to help keep spending down. So I asked the lab’s desk lady how much it would cost through insurance. She said the classic response, familiar to readers of this blog:

“Oh, we don’t know. It’s up to the insurance company – they pay whatever they pay.”

So I called back the insurance company, and told that to the next nice lady, and asked “So, what do you pay?” And she said:

“Oh, we don’t know – it depends what the doctor charges, and your deductible and copay.”

And I said “So in my case, what would that be?” She said there’s no way to know.

Chaos. Behind a veil of secrecy.

Observe, ladies and germs: money flows around, behind a veil of secrecy, and nobody we are allowed to talk to can give us any information so we can make responsible, informed choices.

Where does the money go? Does anyone know? Looking at that cost chart, I’m guessing it’s being shoveled into someone’s pocket, behind that veil. Jerry Maguire shouted “Show me the money”; I’d settle for just being able to watch it move – “Show me the cash flow!”

I say, let patients help control the cost of care. Until then, let’s not let anyone say consumers are the cause of rising costs.

_____________

p.s. As always on these calls, I asked if I could talk to the people who do know, and this time, much to my surprise, she said yes – she gave me the phone number of the company who actually negotiates the prices! This is the first time anyone’s offered it.

Update Nov 2015:

Two additions:

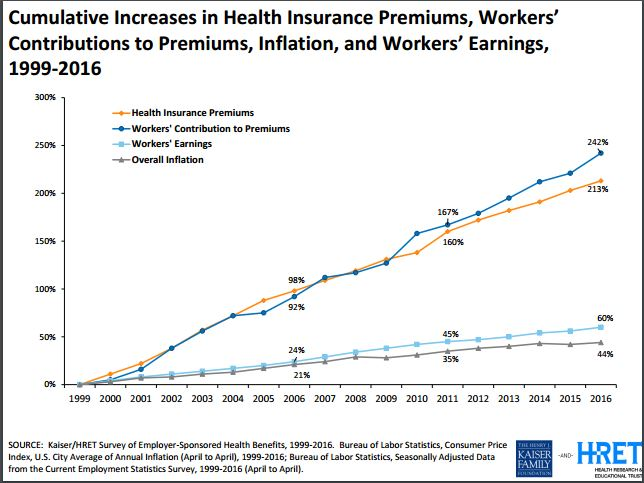

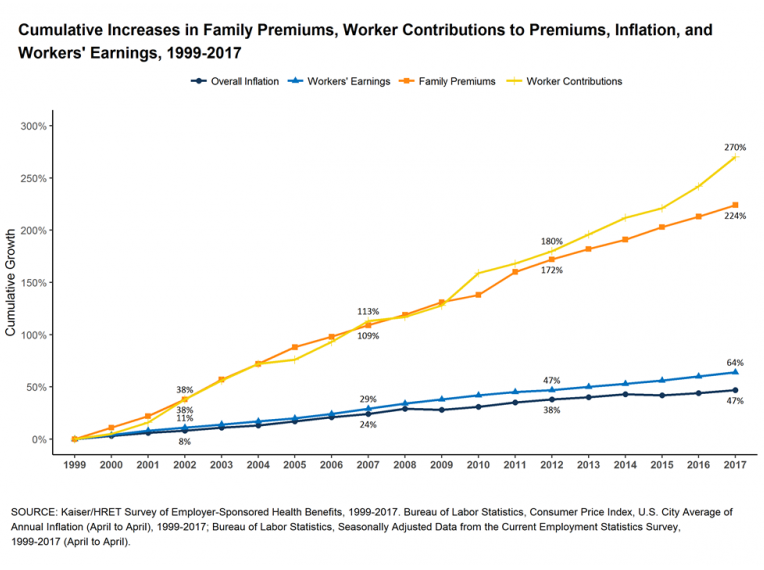

Update 1: The trend continues through 2014 2015 2016

The Kaiser Family Foundation (KFF) slide above shows data through 2012. They publish this yearly, and in some speeches I use one or more. For future reference here’s the complete set, starting from the 2010 edition. Note that the advent of the Affordable Care Act has had absolutely no effect on these trends – it’s what they call an “inexorable trend,” so that’s what I titled the slides.:-) (No effect yet, at least. )

Update 1b: 2016 edition

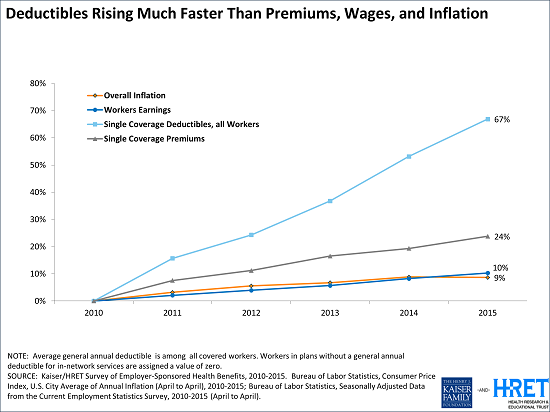

Update 2: Meanwhile, they’re giving citizens more of the burden

The slides above only compare costs against wages – those slides say nothing about what we get for our money. In September 2015 KFF published one that does – the trendline for our deductibles: despite inexorably rising premiums, the insurance industry is also leaving us with more of the bill, by increasing our deductibles.

From the web page with this graphic:

From the web page with this graphic:

Since 2010, Deductibles for All Workers Have Risen Almost Three Times as Fast as Premiums and About Seven Times as Fast as Wages and Inflation

… “With deductibles rising so much faster than premiums and wages, it’s no surprise that consumers have not felt the slowdown in health spending,” Foundation President and CEO Drew Altman said.

“Consumers [that’s you!] have not felt the slowdown” – no kidding! That’s because the money companies are seeing to it that they get their share first. Why this is called “insurance” is beyond me.

I can identify with the frustration. An even more basic problem is “were these lab tests even needed in the first place?”

Consumers cannot be expected to make these determinations, but consumers have a right to know the evidence behind the recommendation to have the test.

Other appropriate questions are ” who makes the profit? ” and “how will this test result change my treatment.”

Far too many tests are done with no indication, raising the concern of financial motivation behind test being ordered. Consumers have a right to understand why these tests are needed and where can they be done at the lowest cost and highest quality.

Michael, in the category of “were these tests even needed” –

1. When I was shopping for a CT last year (because I was newly self-pay), I carefully matched what my hospital had ordered in the past. Because of questions asked by other providers, I discovered that my previous CT had included $400 of lab tests that were not actually needed – they’d just been added. For no reason.

2. 15 years ago, when I was also self-pay, I had what appeared to be a bladder infection. The local walk-in clinic sent out for lab work, which I paid for (cash). When I came back to get the results, the doc said the results were obviously wrong – “Ridiculous,” he said. So I said “I’ll get my money back, right??” And he looked at me like I was nuts.

This is an industry that seems to be in serious need of basic consumer protection. Crazy: the guy said the test was obviously wrong, but it was absurd to want my money back??

This really is not secrecy; it is complexity. The problem for any customer service agent in a plan is that they can (usually) tell you what is covered, but they cant know the status of your deductible. They won’t know that until the claim (and any other potentially concurrent outstanding claims) are adjudicated. That can take weeks (easily). Ergo, even though a service is “covered”, it does not mean that the plan pays. It actually is “decided by the computer” in a practical sense.

Is it that they cannot know the status of your deductible, or that they do not? And in either case, why?

My point, Tim, is that if the people I get to talk to have no idea what’s going on, that’s ridiculous, and it’s not a functioning market.

Once upon a time there were no computers that could dish up the comparative prices of computer products at 17 different vendors. Then that software got written. There’s no reason on earth why the same can’t be done in medicine, and I’m sure it will be, when it becomes a functioning marketplace.

btw, I don’t have access to the full text of Reinhardt’s paper, but I know it applied to things far more insidious than whether a blood test is covered by my insurance… and I imagine you’ve seen the recent publicity about the 25,000 word Steven Brill article in Time this February, “Bitter Pill.”

Excellent news! Uwe Reinhardt’s paper is now available to all. It can be found here: http://content.healthaffairs.org/content/25/1/57.full.pdf+html

As end users, transparency and full disclosure prior to use is a must. We would not accept this system for the sale of a house, car maintenance etc. Those who did this years ago in full good faith for pension plans and money management were the ones whose future was compromised. If we have full transparency in research with all trials registered and reported how much more is this an ethical and practical absolute for our health care. As users we need to advocate, lobby and petition for accountability and transparency (full disclosure) and #WeAreNotWaiting!